Friday, June 12, 2009

RBS WorldPay's Customer Data Security Breach Litigation Transfer Order

RBS WorldPay's Customer Data Security Breach Litigation Transfer Order

Transferred Litigations (.pdfs) | ||||||

MDL No. 2035 -- IN RE: RBS WorldPay, Inc., Customer Data Security Breach Litigation | ||||||

Canada's 3 Largest Get Together for Mobile Payments

By Stefan Constantinescu on Friday, June 12th, 2009

Canada’s three main operators: Bell, Rogers (NYSE: RCI) and Telus (NYSE: TU), are joing forces to launch a mobile payment system called Zoompass.

It’s supposed to be launching on June 15th and will allow customers to send, receive and request money, with a $0.50 fee to send money and transfer funds from your Zoompass account to your bank account. Zoompass is built on EnStream software and that’s just about all the information we have.

The website is blank. Transactions from mobile devices are supposed to reach $1.6 billion this year according to ABI Research,

![Reblog this post [with Zemanta]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_udSp0wf6k0dMSsnwZIz6xWIjPpgkKUwbvbAxhJOF_82hFmFDTAqvwu0kniZCsFbCarD9OvKbvd9VqReoEnV-oMDk6nj60rkjx-6_iVx_VoHZSjSdCyQcBM1WgowKBmDNjzwujCU2f1VQYNgiLqkMQh=s0-d)

Banks Lose $200M Credit Card Case

MONTREAL–Several financial institutions were ordered yesterday to pay more than $200 million to Quebec credit-card holders after a court ruled they broke consumer-protection laws.

MONTREAL–Several financial institutions were ordered yesterday to pay more than $200 million to Quebec credit-card holders after a court ruled they broke consumer-protection laws.Superior Court judge Clément Gascon found that nine banks and financial cooperative Desjardins unjustly charged clients during the conversion process of foreign currencies for credit-card transactions made abroad. The judgment says the charges cannot be billed to consumers before a 21-day grace period.

A class-action suit took aim at institutions that offered Visa, MasterCard or American Express cards between 2001 and 2007. Gascon's ruling ordered each company to pay different sums.

The decision comes a month after federal Finance Minister Jim Flaherty unveiled new rules for credit-card issuers requiring clearer information and a minimum 21-day interest-free period on new purchases made with plastic.

The Canadian Press

Charlie Forte Starting New Payments Initiative

I found this story interesting because HomeATM offers payment processing, real-time money transfers, TRUE PIN Debit for the Web, Two Factor Authentication for online banking and thus bill payment. Eula Adams, former COO of Pay By Touch used to be the CEO of Western Union. Wonder if he's involved...he's in Denver. Either way, Charlie, give us a call, let discuss synergies!

I found this story interesting because HomeATM offers payment processing, real-time money transfers, TRUE PIN Debit for the Web, Two Factor Authentication for online banking and thus bill payment. Eula Adams, former COO of Pay By Touch used to be the CEO of Western Union. Wonder if he's involved...he's in Denver. Either way, Charlie, give us a call, let discuss synergies! Ex-CEO of First Data Corp., makes a power play in Denver - The Denver Post

Charlie Fote, (left) the executive who moved First Data Corp. from Atlanta to metro Denver, is jumping back into the electronic-payments business.

Fote has kept a low profile since November 2005, when he stepped down as chief executive and chairman of the country's largest processor of credit- and debit-card transactions.

The Connecticut transplant helped his son launch a corn and soybean farm in Nebraska, ranched up in Boulder, spent time with his eight grandkids, rode his Harley and golfed with friends. But the hard-charging executive, known for his 6:30 a.m. daily staff meetings, realized he wasn't ready to hang it all up at age 60.

"I was getting bored," he admits.

Fote also saw a confluence of willing investors, eager sellers of payment and transfer companies and unemployed talent in the area.

Over the past eight months, Fote has crafted plans for a new holding company, which will be based in the south metro area.

Using his own money and funds from two or three private equity firms, Fote plans to acquire companies, the first by September, in the electronic-payments and money-transfer business. "It will look like Western Union and First Data put together," Fote said.

Shortly after Fote left First Data, the company's board of directors voted to spin off Western Union into a separate company.

If integrating the two companies was his vision for the future, it wasn't going to be realized. "It will be easier this time to build it the way we want to build it," Fote said. "We have no baggage. We are starting fresh."

Fote said the new company, which doesn't yet have a name, will emphasize what consumers want rather than focusing on technology or payment processing, which is increasingly becoming a commodity business.

One example: Merchants in the new system can offer customers the ability to decide at the register what currency they want to pay with. The conversion will happen at the point of sale.

Nobody is offering an integrated system that can process payments and handle money transfers and bill payment, said Gwenn Bezard, research director of Aite Group, a financial research and advisory firm in Boston.

"It makes a lot of sense as a concept to bring to market something that is integrated," Bezard said. "The concern I have is that merchants already have access to those products." The success of his venture will depend on the willingness of merchants to purchase an integrated package rather than a la carte, Fote said.

Fote is confident he can repeat the success of First Data, which went from $11 million to $11 billion in sales in the three decades he worked there. "You have to have growth," Fote said. "You need a success story."

PayPal Prez: "Great Progress" on Bill Me Later Integration

SAN FRANCISCO -(Dow Jones)- The head of eBay Inc.'s (EBAY) PayPal unit said Tuesday that the online payments group was making "great progress" integrating recently acquired Bill Me Later, which enables online retailers to offer shoppers credit.

SAN FRANCISCO -(Dow Jones)- The head of eBay Inc.'s (EBAY) PayPal unit said Tuesday that the online payments group was making "great progress" integrating recently acquired Bill Me Later, which enables online retailers to offer shoppers credit.PayPal President Scott Thompson said the first phase of the BML integration will be rolled out this summer, with the second phase due to be implemented by the first quarter of next year. He noted that PayPal's margins would take a slight hit over the next two years as a result of the integration, but margins would return to historical norms afterward.

Thompson made his comments at the Credit Suisse Global Media and Communications Convergence Conference, which was Webcast.

The San Jose, Calif., company last year bought Bill Me Later, saying it was a "perfect complement" to PayPal and would increase eBay's exposure to larger online merchants. BML's proprietary underwriting system tells shoppers within seconds if they're approved for credit, without detailed application forms.

Continue Reading at NASDAQ

Global Payments Buys Remainder of HSBC Merchant Services

June 12 - HomeATM PIN Payments Blog: According to reports trickling from the news wires, Global Payments Inc has agreed to buy the remaining (49%) stake in its British joint venture with HSBC Bank Plc for $307.7 million in cash..

June 12 - HomeATM PIN Payments Blog: According to reports trickling from the news wires, Global Payments Inc has agreed to buy the remaining (49%) stake in its British joint venture with HSBC Bank Plc for $307.7 million in cash..Global Payments, which processes online credit card transactions, said it expects the deal to add to its fiscal 2010 results.

It was just a year ago, (June last year) that Global Payments bought a 51 percent stake of HSBC's merchant services division. They paid $439 million for the majority stake in the joint venture to expand and provide payment processing services to merchants in Britain. So either they paid too much for 51%, ($8.6 million per percentage point) or got a helluva deal on the 49% ($6.3 million per percentage point) (or 2% of the HSBS Merchant Services was worth $131.3 million by itself)

Atlanta-based Global Payments said it used existing cash and lines of credit to complete the deal. Shares of Global Payments closed at $37.45 Thursday on the New York Stock Exchange.

Atlanta-based Global Payments said it used existing cash and lines of credit to complete the deal. Shares of Global Payments closed at $37.45 Thursday on the New York Stock Exchange.Here are some additional facts according to the London Bureau of the Wall Street Journal:

- The HMS joint venture was created in June 2008 when HSBC sold a 51% stake to Global Payments Inc., a processor of electronic transactions.

- HSBC and Global Payments also have sale-and-referral agreements in the U.S. and Canada along with a joint venture in Asia covering 11 countries and territories.

- A new 10 year marketing alliance agreement has also been signed, under which HSBC will continue to refer its U.K. customers to HMS.

- No staff will be affected by the change of ownership and HMS will continue to be based in Leicester.

Ganging Up on PCI?

NRF and Other Retail Groups Gang Up On PCI, Demand More Reasonable Rules

Written by Evan Schuman

Representatives of seven of the largest retailer organizations sent a strongly-worded letter to the PCI Council on Tuesday (June 9), asking officially for several major changes to PCI to make compliance an easier goal. The PCI council issued a response, which pretty much amounted to “we like feedback. Have a nice day.”

The letter to the council supported an end-to-end-encryption standard, sought more input from retailers at an earlier stage, asked for larger chains to be given more time to implement new PCI requirements, wanted there to be a list of the most important elements that really need to be done (rather than insisting on compliance with every one of the “more than two hundred detailed requirements of the PCI DSS”) and called for allowing retailers to store fewer pieces of sensitive data.

The letter was written to Bob Russo, general manager of the PCI Security Standards Council, and was signed by National Retail Federation CIO Dave Hogan, National Restaurant Association CEO Dawn Sweeney, Merchant Advisory Group CEO Dodd Roberts, American Hotel & Lodging Association CEO Joe McInerney, International Franchise Association CEO Matthew Shay, National Council of Chain Restaurants President Jack Whipple and the Association for Convenience & Petroleum Retailing CEO Henry Ogden Armour. The letter was cc’ed to American Express CEO Kenneth Chenault, Discover Financial Services CEO David Nelms, Visa CEO Joseph Saunders, MasterCard CEO Robert Selander and JCB CEO Tamio Takakura.

Continue Reading at StorefrontBacktalk.com

![Reblog this post [with Zemanta]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_seCneXQzhsjB0LCu0DrmJ9ggSDOI5xZvkMDdrc3xlKW_DASd8QfpVl-GeRpBpXAKecjR7POGZ-EHkwc1qNnmtZoS-I26kd03oEZ_JhPKu5OtaLfUdWHZ3LJZxiwPcPjFLnHUC0pYSvPZDFrPiftq4=s0-d)

Massive Security Mandates for ATM Deployers in Canada

ATMIA: ATM deployers in Canada buckle down for massive security mandates

ATMIA: ATM deployers in Canada buckle down for massive security mandatesTracy Kitten editor | ATMmarketplace.com

TORONTO — Despite the economy, independent ATM deployers in Canada made the investment this week to attend the ATM Industry Association's annual Canadian show. Attendance numbers for the regional conference hit a three-year high, organizers say — up an estimated 20 percent to 25 percent from 2007 and highlighted by a number of first-time attendees. Attendance topped out at 135, rivaling the conference's best-attended event in 2005, when nearly 200 attendees made their way to the show.

Perhaps Canada's push for upcoming anti-money-laundering regulation and looming deadlines for EMV compliance spurred interest among IADs, which now more than ever are looking to industry associations such as ATMIA to lend a hand and a voice.

The conference theme, "Turning Challenges into Business Opportunities," could not be more fitting, or timely, says Gary Ferris, an independent financial services consultant and the show's emcee. IADs in particular are being called to change the way they view and do business, he said.From a security perspective, Interac, which recently announced plans to become a private, for-profit entity, is pushing IADs against the wall, say independent operators Clifford Richstone and Chris Chandler. Interac, as Canada's primary ATM and POS network, has a stronghold on the market. And mandates passed down by Interac must be complied with.

Having a single network has its benefits and drawbacks, industry insiders agree.

From an EMV and compliance perspective, a single point of contact has been advantageous, says Wendy Macpherson of Interac. The country's ongoing conversion from the magnetic strip to chip and PIN has been relatively painless, because Interac has been able to set deadlines, guidelines and mandates without the need for a lot of collaboration between networks, switches and processors — collaboration that will be a necessity in the United States, should the U.S. ever take the EMV plunge.

In fact, the United States' diversity and complex infrastructure of networks, processors, etc., is often blamed for its resistance to EMV migration. That market complexity, experts like Macpherson argue, likely has left many U.S. FIs disillusioned about how much ATM and debit-card fraud is actually impacting them.

"With so many small FIs and networks, I think there could be more fraud in the U.S. than the banks realize," she said.

Continue Reading at ATM Marketplace

Ingenico Sells Denmark and Finland Entities to BBS

Ingenico announces the sale of SAGEM DENMARK and MANISON FINLAND to BBS

Ingenico announces the sale of SAGEM DENMARK and MANISON FINLAND to BBSIngenico announces today the sale of Sagem Denmark and Manison Finland to BBS, a leading provider of electronic ID, payment and information solutions in the Nordics. The sale is combined with the signature of a strategic partnership with BBS for the distribution of Ingenico's Telium based terminals in this region.

Following the transaction that will be in cash, BBS will hold 100% of these two entities which contributed, in 2008, in revenue of EUR 39.1 million and operating margin of EUR 4.6 million. The closing of the transaction should take place in the next 60days.

Philippe Lazare, Ingenico Chief Executive Officer, commented: "The disposal of these two companies acquired as part of the transaction of Sagem Monetel is an opportunity to withdraw from non strategic activities but also to reinforce our commercial position in Nordic countries thanks to BBS leadership in this region. This disposal also very substantially strengthens our liquidity position and thus, our strategic flexibility."

Ola Forberg, BBS Chief Executive Officer, added: "Ingenico has been a strategic partner within the area of payment terminals for several years. This acquisition is important for us to achieve our ambition of becoming the leading provider of merchant solutions in the Nordics. With this acquisition we have strengthened our co-operation with the world's leading provider of payment solutions."

About Ingenico (ING)

Throughout the world, banks and retailers rely on Ingenico for secure and expedient electronic transaction acceptance. Ingenico solutions leverage proven technology, established standards and unparalleled ergonomics to provide optimal reliability, versatility and usability. This comprehensive range of products is complemented by a global array of services and partnerships, enabling businesses in a number of vertical sectors to accept transactions anywhere their business takes them. For more information about Ingenico, please visit: www.ingenico.com.

Thursday, June 11, 2009

iTunes & Amazon Targeted in Credit Card Fraud Scheme

Amazon & iTunes Targeted in £470,000 Credit Card Fraud - ITProPortal.com

Amazon & iTunes Targeted in £470,000 Credit Card Fraud - ITProPortal.comAmazon & iTunes Targeted in £470,000 Credit Card Fraud

A gang of nine have been arrested after they were accused of downloading their own tracks off Amazon and iTunes using stolen credit card details AND then claiming royalties on that.

The scam involved recording 19 song compilations, uploading them to the aforementioned online music stores at a cost of £18 each by using a New York-based online music store intermediary.

The lot then created up to 1500 iTunes and Amazon accounts using stolen US and UK credit card details before setting out on a massive spending spree that saw them spend nearly £470,000 on buying their own album.

Having purchased around 75,000 of their own albums, they also raked in significant royalties - which amounted to an estimated £400,000 - and the sales allowed them to rise rapidly in the charts. The con was only spotted when credit card companies became suspicious over the transactions.

The nine involved are all based in UK and are being held "on suspicion of conspiracy to commit fraud and money laundering". Up to 60 officers have been involved in coordinated raids and were led by Scotland Yard's E-Crime Unit.

Continue Reading

PayPal Blog - Now Available on American Airlines & Emirates Airlines in UK

The PayPal Blog » Blog Archive » PayPal Now Available on American Airlines and Emirates Airlines in the UK

The PayPal Blog » Blog Archive » PayPal Now Available on American Airlines and Emirates Airlines in the UKHi everyone. I¹m Cameron McLean, PayPal¹s General Manager for UK Merchant Services. With the summer holidays fast approaching, many families are planning their summer getaways. While traveling abroad with the family inevitably requires some extra patience, booking your tickets in the first place shouldn¹t, which is why I¹m delighted that customers of American Airlines and Emirates Airlines in the UK can now speed through checkout as quickly as their cousins across the pond, by paying via PayPal.

Customers paying for Emirates or American Airlines flights through PayPal won¹t have to enter any financial or billing information, making booking flights faster and easier. What¹s more, UK residents will be able to pay for flights on www.emirates.com or www.aa.com using PayPal with the flexibility to fund their tickets via PayPal balance, along with local payment methods such as UK debit cards and local bank account funds, a move we expect to be really popular with American Airline¹s and Emirates customers.

Emirates joined PayPal following some interesting customer research on which alternative payments methods are likely to most appeal to customers in over 37 countries served by the site. We¹re delighted that, unsurprisingly, PayPal was at the top of their list!

Paying for Paying with Plastic

The Government Accountability Office has been ordered to study the use of credit by consumers, and in particular the effect interchange fees have on consumers and merchants.

Many people may not be aware of these fees, but for lenders, merchants and consumer advocates, the fees are the next controversial credit-related issue Congress may take up.

An interchange fee is paid by a merchant's bank to a customer's bank or credit union when the business accepts purchases by credit or debit cards. Typically the fees are 1 to 2 percent of the total cost of a purchase. For example, if a consumer buys $100 of merchandise or services, the interchange fee paid by the merchant could be $2.

This may not seem like a lot of money, but multiply that by the millions of people making electronic purchases and it's not chump change. Moreover, everybody pays, whether you use plastic or not, according to consumer advocates and retailers. The interchange fees result in higher prices for everyone, including those paying with cash.

The Credit Card Accountability, Responsibility and Disclosure Act that President Obama recently signed into law includes a provision to investigate the fees that businesses pay to allow their customers to use credit. The idea is to provide more transparency to consumers.

Demanding that credit card companies give more information about interchange fees would put them on par with food producers who are required to provide nutritional information on packaging. The nutritional details are meant to help people make healthier choices. And yet Americans are fatter than ever.

The same can be said about our appetite for credit.

Continue Reading at the Washington Post

Microsoft Money Shelved

| Important notice: Microsoft Money Plus will not be available for purchase after June 30, 2009. All purchased Money Plus products must be activated prior to Jan. 31, 2011. With banks, brokerage firms and Web sites now providing a range of options for managing personal finances, the consumer need for Microsoft Money Plus has changed. After suspending annual updates of Money Plus in 2008, Microsoft is announcing today that we will no longer offer Microsoft Money Plus for purchase after June 30, 2009. We would like to thank the many dedicated users who have been enthusiastic supporters of Microsoft Money over the years, as well as our partner financial institutions who helped pioneer a digital vision of financial management. Microsoft remains committed to helping customers chart a course to financial well-being. The MSN Money Web site will continue to provide personal finance information and advice plus comprehensive market news and quotes. We will continue to evolve and enhance the online MSN offering in the coming months. Current Money Plus customers who have questions or concerns can find additional information here. Additional Content

| |||||

Doctors Operate Without Interchange Fees

Rising Fees Could Be Culprit As Fewer Doctors Accept Credit Cards

While credit card acceptance is making inroads in a slew of new markets like transit and parking, it turns out the plastic is losing ground among physicians.

Some 32.7% of doctors’ offices do not accept credit cards, up almost 4.5 percentage points from a year ago, according to a survey from SK&A Information Services Inc., a research firm specializing in health care.

Rising interchange rates may be to blame, according to Jack Schember, director of marketing for the Irvine, Calif.-based company, which surveyed physicians in April following its first survey in April of last year.

Continue Readinig at Digital Transaction News

Minnesota Calling Off Online Gambling Dogs? You Betcha!

Minnesota (Land of the Loons) Withdraws Planned Internet Gambling Blackout

Minnesota (Land of the Loons) Withdraws Planned Internet Gambling Blackout The Minnesota Department of Public Safety’s Alcohol and Gambling Enforcement Division has sent letters to 11 of the world’s largest internet service providers (ISPs) rescinding its notice to block 200 internet gambling websites.

In April, John Willems, Director of the Alcohol and Gambling Enforcement Division (DAGED), served notice to 11 ISP’s calling for the blockage of 200 gambling sites to Minnesota residents.

These threats have been rescinded and no action will be taken to block internet gambling sites in the state.

The withdraw is down to the Interactive Media Entertainment and Gaming Association (iMEGA), who, shortly after the list of 200 sites was made public, filed a lawsuit against Willems and his actions. iMEGA charged that Minnesota did not have jurisdiction to act and the State’s actions represented a breach of the Commerce Clause of the United States Constitution.

In response to The Gambling Enforcement Divisions wanted crackdown iMEGA outlined their stance in a letter to the ISPs themselves.

“Because website operators are not subscribers of yours, have no contracts with you, and are not provided facilities by you, you should be aware that the Minnesota Department of Public Safety is attempting to mislead you into believing you are bound by federal law.”

You Betcha!

![Reblog this post [with Zemanta]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vCbvW3Nkh2mLlRKXhKe2CUvBT8o5wAgVjCJlVl6-wrGMRf5uc8dz4x5Uawun7WShbzu-aS_BYUDEHENWo-Z_x3jNl0p8JrfCtJhMpcUMWoY6qsKEq-h6Lo0NYCHFgquXkKkLDmxNOo0BYivt_lXEc=s0-d)

The (P)assword Is: Oxymoron

Online transaction security: Tips for staying safe

Online transaction security: Tips for staying safe By Alex Kidman on 09 June 2009

The online economy is massive, with billions of dollars changing hands every single day. Online shopping has brought consumers lower prices, incredibly diverse choice and an ease of buying that simply can't be matched in the physical world.

At the same time, however, it's not without its perils. Any time that much money is changing hands on a regular basis, there will be sharks circling trying to snap off a chunk of cash.

Consultants QPR recently released a report into credit card fraud in which they estimated the cost of "Card Not Present: fraud in Australia (which logically includes all internet-based transactions) was a problem worth $71,578,908 in 2008, a rise of 33 per cent over the previous year.

So, online buying presents challenges to keeping your money safe, but if you're smart, they're challenges that aren't too hard to overcome.

Online banking

Banks love online banking; it's cheaper for them to deliver than over-the-counter services, and the convenience of being able to check your balances, transfer funds and pay bills online make it a real winner for consumers as well. The Commonwealth bank, for example, is reported to have at least 2.6 million active online banking customers, with a take-up rate of 60,000 more each month.

In order to access your online banking, you typically need your account number and a password. Needless to say, it's a very bad idea indeed to write your password down somewhere that somebody might find it. That doesn't have to be the end of your banking security, however.

To access your account, you'll typically need an username or client number and a password Some banks extend their security with additional measures, which range from floating on-screen keyboards (which stop automatic attacks that rely on the position of the entry field being absolute) to the ability to have a secondary code automatically generated, either via a security dongle the bank supplies, (Question: If you hook up your dongle to your Blackberry would it be called a dongleberry?) or even by having the code sent via SMS to your mobile phone.

But when it comes to providing security never forget these eight words:If you type it...hackers can swipe it.

Editor's Note 2: I have a better idea. Lets Keep It Simple...how about taking out your bank issued card, swiping it and then entering your bank issued PIN? No card, No PIN, No access. Sealed with KISS.

Continue Reading at cnet Australia

![Reblog this post [with Zemanta]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_u0ecDuDisSeBRSDJl-207SrrxpXUk9qroPvisj5aUzwnWmhM1rpc2sL1QLcEtuiqhRj1KrzABtykhAmSjIJQTm7YboGvs-MWyA-LRyAfOWj-GhMjT8f8JjIk3KXBOl3wY4vPty37nWdUvN6r-_Gv3S=s0-d)

More On ATM Malware from McAfee Blog

ATM Malware Makes Withdrawals in Russia

Francois Paget

Trackback

We frequently encounter password stealers and backdoors in computers after their owners have browsed unsafe websites or opened unknown email attachments. It is more unusual, however, to see these malware directly implemented in banks’ automated teller machines. In these cases, Trojans have to be installed by people who have physical access to the machines. Data collecting and malware removal would need yet another visit or visits. It should seem obvious that such malware installation requires a high level of “cooperation” from the bank staff.

One of the first attacks occurred in Russia more than one year ago. It was announced in January 2009 when Diebold Inc. released a security fix for its Opteva Windows-based ATMs. At that time, the company said some suspects were apprehended. But it seems the gang was not fully dismantled. In May, we heard of new suspicious files discovered in Eastern European ATM machines. The security firm Trustwave published a study concerning this matter. The software had been updated and new virtual robberies had been launched.

On June 3, The Register also raised public awareness by covering the story. When active, the Trojan intercepts transactions and records them on log files. To control an infected ATM, the attacker uses dedicated credit cards that allow him to activate some administrative rules. Via the ATM’s display, he can select various options from the keypad to display statistics (numbers of transactions, cards, keys), print collected data, force the machine to dispense all its cash, uninstall the malware set, and reboot the ATM.

Continue Reading

![Reblog this post [with Zemanta]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vxHz0eSw3JImWwrwgjNnbEcIKVR8cClohcsHx9Julx4gsQA24XWJ767870Dw-qU4_ayx8RZMT697s3fY9XgjbEpbRrVEBw63K_UJGnAxfrBLELgaPGOG0q-F6N5X9dNnzqhxtqDyAAXa3SlBo_3mR4=s0-d)

Spam with Eggs Maybe...Just Not with Mobile e-Mail

Japanese Mobile Moves Online

Japanese Mobile Moves Online

JUNE 11, 2009

E-mail is important, too.

For many years the mobile market in Japan has served the rest of the world as a model of the future of mobile development. If that holds true, expect more mobile users online.

According to the Japanese Ministry of Internal Affairs and Communications, mobile Internet in Japan reached nearly 83% penetration among mobile phone users.

A total of 75.1 million users in Japan accessed the Internet via mobile phones in 2008.

One of the most popular mobile phone activities for young adults in Japan was e-mail, with 72% of users ages 8 to 24 reading and answering e-mails on the go.

Japan’s culture of connectivity pushed penetration far above the 13% average for Asia-Pacific, according to a Synovate study sponsored by Microsoft Advertising, MTV and Yahoo!. Marketers should be cautious about tapping into this tech-savvy demographic with tried-and-true e-mail marketing, however.

According to a survey by Point On Research, 86% of mobile phone users in Japan check their e-mail every day—but they are highly sensitive to spam. Mobile spam was seen as unsettling by more than 85% of respondents surveyed by goo Research.

The same survey found that 33% of those users received at least one piece of spam in their mobile e-mail each day.

Mobile marketing campaigns should take a more personal route. “The ability to stimulate user action will be the key to success in mobile advertising,” said Yeunsil Lee, an ROA Group analyst.

Just don’t “stimulate” them with anything that looks like spam.

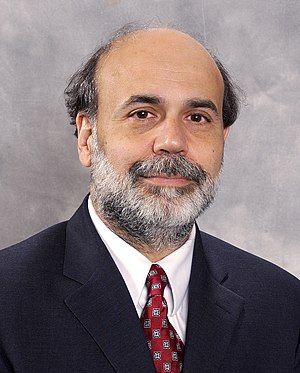

Bank of America Pressured by Feds to Buy Merrill Lynch?

Documents released by Republicans paint a not-so-flattering portrait of federal regulators exerting pressure on Bank of America to conclude its deal with Merrill Lynch, even though the the deal was fast deteriorating. Bank of America CEO Ken Lewis testified that federal officials pressured him to the point that his job was at stake.

Reuters notes an email from Richmond Fed President Jeffrey Lacker that cites Fed Chairman Ben Bernanke on Lewis' belief that he could exercise a "material adverse change" (MAC) clause to scuttle the Merrill agreement. "Just had a long talk with Ben...Says they think the MAC threat is irrelevant because it's not credible. Also intends to make it even more clear that if they play that card and they need assistance, management is gone."

The New York Times suggests the government was alarmed as Merrill's condition weakened. They hashed out a plan to save Merrill in the event the deal fell through. The news coincides with the House Oversight and Government Reform Committee hearing today. It will feature Lewis as the sole witness and examine the deal.

For more:

- here's the Reuters article

- here's the New York Times article

![Reblog this post [with Zemanta]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_uWu7z71b2eyRovGfa3xPykOpQeJF_7O27OCnI0KsaVRpsOvTb7CnE-SlxsuUPcuzI0QlvcOu18Y1EQ8jPTPGRYtyDzsLFT9kv5VPT_4QUggQVQHjRj5S1TMtwDI9bdP0urRxQSmyPNEKBTI1-KCGZt=s0-d)

Subscribe to:

Posts (Atom)